Featured Graph

Excerpted from TFI's report:

Transforming the Local Exchange Network: Third Edition

Lawrence K. Vanston, Ph.D. and Ray L. Hodges

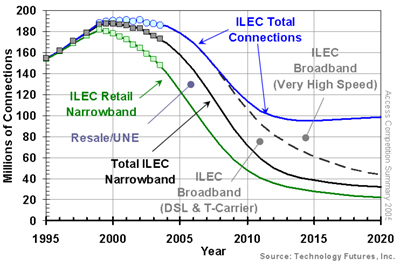

ILEC Narrowband Access Lines and Broadband Connections

A key driver for change is the loss of ILEC narrowband access lines due to competition from wireless, broadband, cable telephony, and VoIP. As illustrated in the figure above, since the peak in 2000 ILEC access lines (including resale and UNE) have fallen from a peak of 187 million in 2000 to 169 million at year-end 2004. The total is forecasted to fall to 71 million by 2010. As can be seen in the figure, ILEC broadband has made up for, and will continue to mitigate, the loss of narrowband access lines_assuming ILECs remain competitive in broadband. Thus, competition has thrust broadband into center ring and made it the basis of survival.

Also shown in the figure above is the expected transition from today's ILEC broadband service (DSL operating at a nominal 1.5 Mb/s) to very-high-speed (VHS) broadband operating at 24 Mb/s and above. The demand for VHS broadband will reflect the general performance increase in computers, i.e., Moore's Law, and the tendency of applications to use it, as well as the specific requirements of IP video.

Please visit the report page, Transforming the Local Exchange Network: Third Edition for more report information and purchasing details.